We examine the recent central bank policies and the impact of Donald Trump’s policies from the SGD-based investors’ perspective.

The Fed

The recent strength in the US economy has given the Fed reasons to be on pause, with the FOMC (Federal Open Market Committee) not in a hurry to continue their rate cut cycle which started in September 2024. After a rate cut of 100 basis points, the Fed now prefers to choose a wait-and-see approach to observe further progress on inflation. Fed’s preferred measure of inflation, Core PCE (Personal Consumption Expenditures) was 2.8% in December 2024. While this seems to be almost at the Fed’s 2% target, the last 80 basis points of improvement has been challenging with Core PCE hovering at these levels for the last 9 months (Figure 1). The recent strength in the US labour market provides further evidence that the current level of interest rates is no longer restraining the economy as much as they had been a year ago. The pause also gives time for the Fed to evaluate President Trump’s policies on immigration, tariffs, taxes and deregulation and how they may impact the economy.

Figure 1: Fed’s Core Inflation Indicators - US inflation data still elevated but on track to the Fed’s 2% target

Figure 1: Fed’s Core Inflation Indicators - US inflation data still elevated but on track to the Fed’s 2% target

Source: Bloomberg, February 2025

Impact of Trump's Policies on Interest Rates

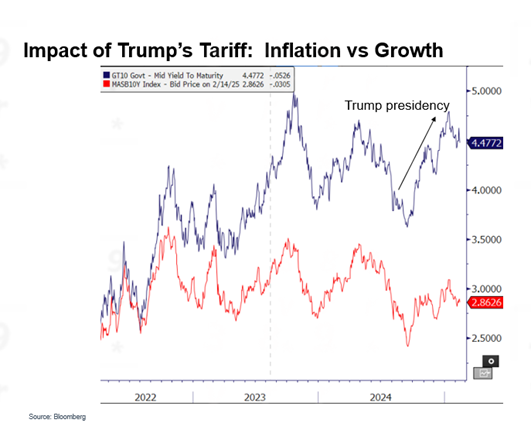

Before the election, bond markets were already concerned about Trump’s potential victory. The US 10-year yield started rising in September 2024 as the chances of Trump becoming US President started to increase (Figure 2). Singapore interest rates followed in tandem, albeit on a smaller magnitude. Markets were concerned about his pro-business and inflationary policies with regards to immigration, taxes, tariffs and deregulation.

Figure 2: Impact of Trump’s Tariff - Inflation vs Growth (US and SG 10-year government bond yield)

Figure 2: Impact of Trump’s Tariff - Inflation vs Growth (US and SG 10-year government bond yield)

Source: Bloomberg, February 2025

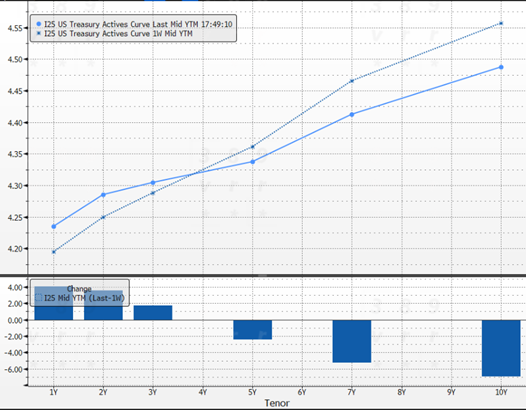

Since assuming office, President Donald Trump wasted no time in following up with his election promises to put in place his policies. To date, he has threatened 25% tariffs on Mexico and Canada (delayed by a month) and a 10% tariff on China. Most recently, he pledged to impose reciprocal tariffs on US trading partners. These actions have introduced volatility in the bond market, causing short-end of the yield curve to rise due to inflation concerns, while long-end of the yield curve to drop due to growth fears.

Figure 3: Impact of Trump’s Tariff - Inflation vs Growth

(comparison of US yield curve prior to Trump’s announcement on tariff on Mexico and Canada and 1 week after)

Since assuming office, President Donald Trump wasted no time in following up with his election promises to put in place his policies. To date, he has threatened 25% tariffs on Mexico and Canada (delayed by a month) and a 10% tariff on China. Most recently, he pledged to impose reciprocal tariffs on US trading partners. These actions have introduced volatility in the bond market, causing short-end of the yield curve to rise due to inflation concerns, while long-end of the yield curve to drop due to growth fears.

Figure 3: Impact of Trump’s Tariff - Inflation vs Growth

(comparison of US yield curve prior to Trump’s announcement on tariff on Mexico and Canada and 1 week after)

Source: Bloomberg, February 2025

Market Reaction to Trump and the Fed

While the market is concerned about the inflationary impact of Trump’s policies, it is important to note that he is aware of the negative impact of inflation on ordinary Americans. Indeed, Scott Bessent, Trump’s newly appointed Treasury Secretary has made it known in several recent interviews that the Trump administration will be keen to bring down inflation. Trump’s use of tariffs may also be less aggressive than feared, as it could be a negotiation tactic with trade partners.

Nevertheless, the bond market has reacted to both the Fed’s pause and Trump’s policies, with Fed Fund Futures market pricing in slightly more than 1 cut for 2025 and another cut for 2026. This is a sharp reduction from September 2024 where market was pricing in a total of 6 cuts for 2025 and 2026. Reflecting this, the 5-year US Treasury rate has risen 90 basis points from 3.4% in September 2024 to 4.3% in February 2025.

Nevertheless, the bond market has reacted to both the Fed’s pause and Trump’s policies, with Fed Fund Futures market pricing in slightly more than 1 cut for 2025 and another cut for 2026. This is a sharp reduction from September 2024 where market was pricing in a total of 6 cuts for 2025 and 2026. Reflecting this, the 5-year US Treasury rate has risen 90 basis points from 3.4% in September 2024 to 4.3% in February 2025.

MAS Policy

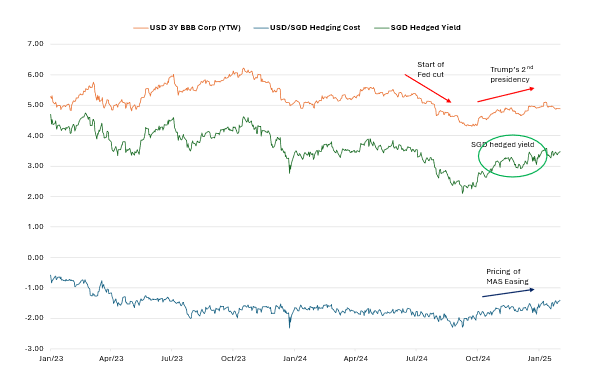

In January 2025, the MAS eased monetary policy by slightly reducing the slope of the S$NEER policy band. The combination of moderating inflation (core inflation expected to be below 2%) and slower growth momentum enabled the central bank to pursue such a policy. The MAS is also assessing the implications of Trump’s policies on Singapore’s economy.

This easing in monetary policy has led to a narrowing of the interest rate differential between US dollar and Singapore dollar, reducing the cost of hedging US dollar assets to Singapore dollar. As seen from Figure 4, the cost of hedging had started to decrease in October 2024 as the market had started to anticipate such a move from the MAS. The cost of hedging has decreased from around 1.8% to as low as 1.4% in January 2025. The lower cost of hedging implies that US dollar assetshedged to Singapore dollar would look more attractive.

Figure 4: Yield of 3yr BBB Corp hedged to SGD

This easing in monetary policy has led to a narrowing of the interest rate differential between US dollar and Singapore dollar, reducing the cost of hedging US dollar assets to Singapore dollar. As seen from Figure 4, the cost of hedging had started to decrease in October 2024 as the market had started to anticipate such a move from the MAS. The cost of hedging has decreased from around 1.8% to as low as 1.4% in January 2025. The lower cost of hedging implies that US dollar assetshedged to Singapore dollar would look more attractive.

Figure 4: Yield of 3yr BBB Corp hedged to SGD

Source: Bloomberg, February 2025

Investment Implications

The Fed’s wait-and-see approach on rate cuts, combined with the market’s concern over Trump’s inflationary polices, have led to interest rates retracing higher from about 6 months ago. We believe the shorter part of the yield curve looks attractive.

In addition, US dollar bonds hedged to Singapore dollar now looking less expensive from 6 months ago as a result of higher US rates and cheaper hedging cost.

Therefore, we believe a portfolio of Singapore dollar and US dollar investment-grade equivalent rated bonds in the 3 to 5 year duration range could potentially offer a yield of 3.7%, making it an interesting investment proposition for Singapore based investors.

All data are sourced from Lion Global Investors and Bloomberg as at 14 February 2025 unless otherwise stated.

Download ReportIn addition, US dollar bonds hedged to Singapore dollar now looking less expensive from 6 months ago as a result of higher US rates and cheaper hedging cost.

Therefore, we believe a portfolio of Singapore dollar and US dollar investment-grade equivalent rated bonds in the 3 to 5 year duration range could potentially offer a yield of 3.7%, making it an interesting investment proposition for Singapore based investors.

All data are sourced from Lion Global Investors and Bloomberg as at 14 February 2025 unless otherwise stated.